Question:

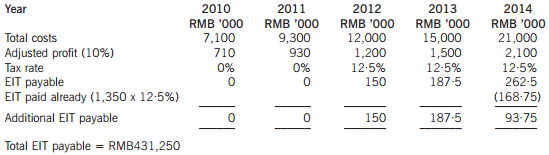

Taip Ltd is a foreign investment enterprise which has been a qualified software enterprise for enterprise incometax(EIT) since its inception in 2010. Taip Ltd produces software products in Mainland China and exports these products to associated companies in the Hong Kong Special Administrative Region for further sale to European customers. Taip Ltd‘s total costs, profits/(losses) and applicable tax rates are summarised below:

In 2015 the tax authorities conducted a transfer pricing audit and concluded that Taip Ltd should adjust its profit based on a mark-up of 10% on total costs for all five years, 2010 to 2014.

Required:

(a)List the four methods (other than cost plus) which the tax authorities can use for transfer pricing adjustments.

Note:No mark will be given for stating ‘other method’.

(b)Calculate the total amount of additional enterprise income tax (EIT) payable by Taip Ltd for the years 2010 to 2014 inclusive.

Answer:

Taip Ltd

(a)In addition to the cost plus method, the following four methods can be used for transfer pricing adjustments:

-Comparable uncontrolled price method

-Resale price method

-Transactional net profit method

-Profit split method

(b)Additional enterprise income tax (EIT) payable for the years 2010 to 2014

,我们将会及时处理。

,我们将会及时处理。